Prefunding Is Costing You More Than You Think

It's Friday afternoon and someone on the treasury team notices the GBP settlement account is running lower than expected. They could top it up, but the banking cut-off has already passed and the next settlement window isn't until Monday morning. Nothing is actually wrong, but nobody wants to be in that position. So the team does what almost every payments business does: they make sure the buffer is large enough that this never becomes a problem in the first place.

Every payment institution, BIN sponsor and multi-currency PSP has lived some version of this. Over time, the buffer becomes part of the operating model. It sits there quietly in the background, rarely discussed and rarely challenged. Most teams think about it as a necessary safeguard rather than a treasury decision. The reality is that what started as protection against settlement timing has become a permanent capital requirement.

The logic behind the buffer

The logic behind it is completely understandable. Visa and Mastercard settle on fixed schedules. Bank transfers have cut-off times. Weekends and bank holidays create periods where liquidity simply cannot be moved, regardless of what is happening elsewhere in the business. As a result, treasury teams don't size liquidity for normal operating conditions. They size it for the worst case: the long weekend, the delayed top-up, the unexpected spike in volume, or the corridor that suddenly needs funding when no banking rails are available.

The result is that most programmes carry significantly more liquidity than they need on an average day. Not because treasury teams are inefficient, but because the underlying rails leave them little choice. If the cost of running short is high, the rational response is to maintain a larger buffer. The challenge is that very few organisations have ever stopped to calculate what that decision is actually costing them.

The cost that rarely gets calculated

When treasury teams talk about prefunding, they often focus on the operational burden. They think about monitoring balances, managing top-ups, handling weekend coverage and dealing with exceptions. Those costs are real, but they are usually not the biggest ones. The larger cost is the capital itself.

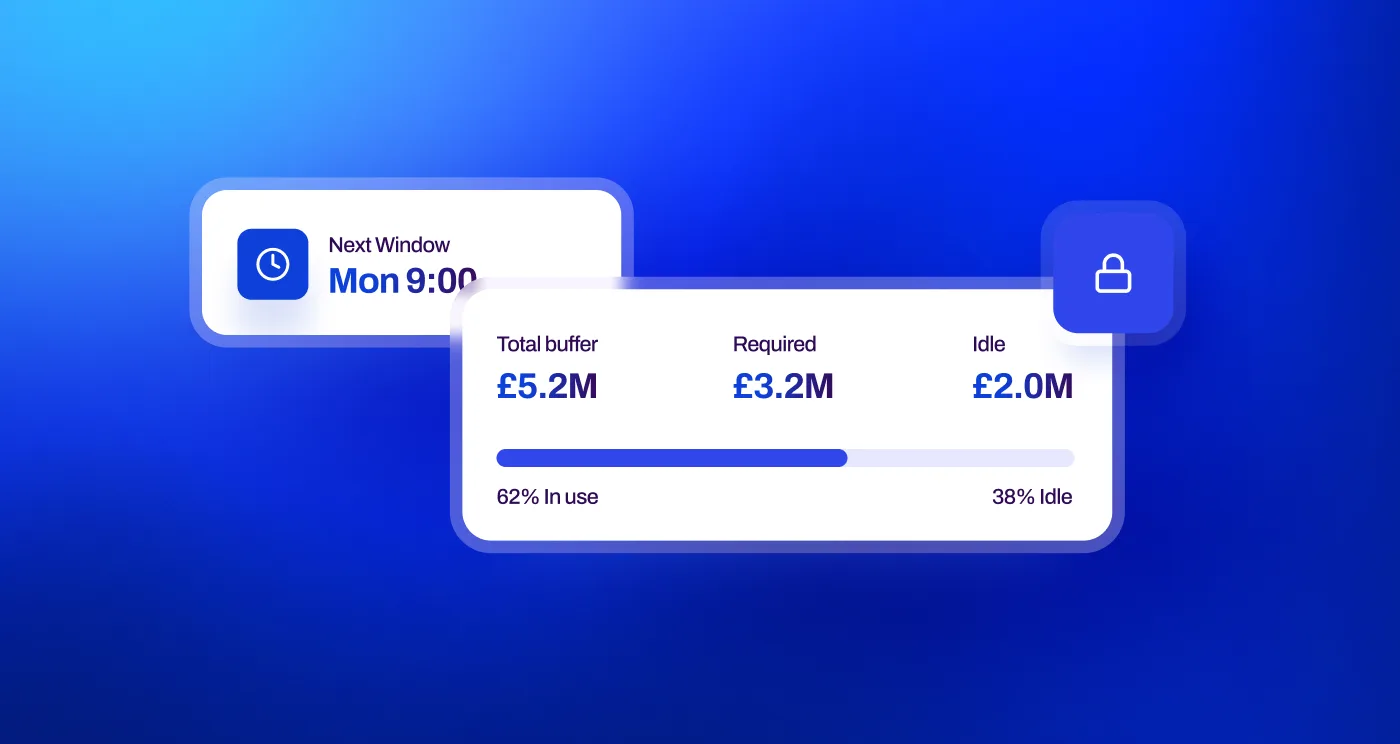

Consider a business holding £5 million of aggregate prefunding across its settlement corridors. Assuming a 5% cost of capital, that represents roughly £250,000 per year tied up purely to support settlement timing. Increase that buffer to £20 million and the number becomes £1 million annually. Nothing has gone wrong, no losses have been incurred and no explicit fees have been charged. The capital is simply unavailable for anything else.

Many firms finance part of this requirement through credit facilities rather than internal capital. While this can reduce the direct opportunity cost, it introduces another layer of expense. Banks are effectively lending against settlement activity they cannot observe in real time, which means uncertainty gets reflected in pricing, covenants and operational overhead. Most organisations end up with a combination of internal capital and external funding, creating a cost that is spread across multiple teams and multiple budgets. Because nobody sees it as a single line item, it rarely receives the scrutiny it deserves, though the cost of capital is often estimated to be around 8-10% annually (1).

Multi-currency programmes compound the problem

The economics become even more pronounced as programmes expand internationally. A business operating in GBP, EUR and USD is not holding one liquidity buffer, it is holding three. Add AUD, SEK or CHF and the complexity compounds further. Each corridor has different settlement timings, different banking cut-offs and different holiday calendars. Because liquidity cannot be moved quickly enough between them, every corridor effectively needs to be funded independently and sized for its own worst-case scenario.

This is where the aggregate cost starts to become meaningful. Treasury teams often assume that these buffers are simply part of operating a global programme, but that assumption is largely a consequence of the infrastructure available to them. The requirement is not driven by customer demand or transaction volume. It is driven by the gaps in the underlying settlement rails.

What stablecoins change

What has changed over the past few years is not the treasury problem itself. Treasury teams still need liquidity in the right place at the right time. What has changed is the funding layer available to solve that problem.

Stablecoins allow liquidity to move continuously rather than only during banking hours. A USDC transfer does not stop because it is Friday evening, and it does not wait for a Monday settlement cycle or a bank holiday to pass. Liquidity can be repositioned in minutes rather than days. That does not eliminate the need for treasury management, but it does materially reduce the amount of capital that needs to sit idle as protection against settlement timing risk.

The first impact is usually a reduction in buffer requirements because the longest funding gaps disappear. The second is that liquidity can increasingly be managed as a pooled reserve rather than as isolated balances across multiple corridors. Instead of maintaining peak liquidity in every market simultaneously, businesses can manage capital centrally and direct it where it is needed in real time.

What the numbers look like in practice

Consider a programme operating across GBP, EUR and USD with £8 million of aggregate prefunding. Under traditional settlement rails, that buffer is largely driven by funding windows, cut-offs and timing risk across each corridor. With stablecoins acting as the funding layer, the requirement may fall closer to £4–5 million because liquidity can move continuously and be managed centrally. The exact numbers vary by programme, but the direction is consistent: the less time liquidity spends trapped by settlement windows, the less liquidity you need overall.

The question worth asking

The most useful question treasury teams can ask is not whether they have enough buffer. It is how much that buffer is costing them. Most organisations know how much liquidity they hold. Far fewer understand the annual cost attached to it, whether through opportunity cost, financing costs, FX exposure or operational overhead.

For years, prefunding has been treated as a fixed cost of operating a payments business. Increasingly, it is becoming clear that it is not a fixed cost at all. It is the cost of operating on a particular set of rails. As new funding and settlement models emerge, that assumption is becoming worth revisiting.

Source & Disclaimer(1): Bitso Business Report, showing an illustrative scenario based on certain operating assumptions and not representative of all programmes