Executive Summary

Stablecoins have moved beyond experimental infrastructure and web3-native use cases, and now have the capability of powering B2B finance, commerce, and treasury securely and at scale.

Over the last two years, we have seen stablecoins explode to support nearly $400bn in real-world payment flows; including B2B transactions, payouts, remittances, and card-linked spend (excluding trading activity). Today, stablecoins are increasingly embedded within traditional financial systems and used by global businesses to reduce FX friction, accelerate settlement, and simplify complex cross-border money movement.

Stablecoins now rival the world’s largest payment networks in transaction volume

What has changed is not the underlying technology, but the scale of adoption, growing regulatory clarity, and the role stablecoins now play within the payments and treasury stack.

Adoption is no longer driven by speculative activity, but by real businesses seeking solutions to challenges in the legacy system: persistent FX inefficiencies, slow and opaque settlement, and fragmented treasury structures. As a result, stablecoins are increasingly treated as payments infrastructure, particularly by businesses operating internationally at scale.

Stablecoins are not a silver bullet, and they are not appropriate for every payment flow. Used selectively, however, this new technology can remove structural friction from specific parts of the money-movement lifecycle.

This guide is designed to help you:

- Assess whether stablecoins address your specific pain points

- Identify potential use cases

- Understand the regulatory and operational considerations

- Evaluate implementation realistically

What Problems Can Stablecoins Solve

Before evaluating new infrastructure, it's important to understand where payment timing, cost, and operational complexity are already affecting your business.

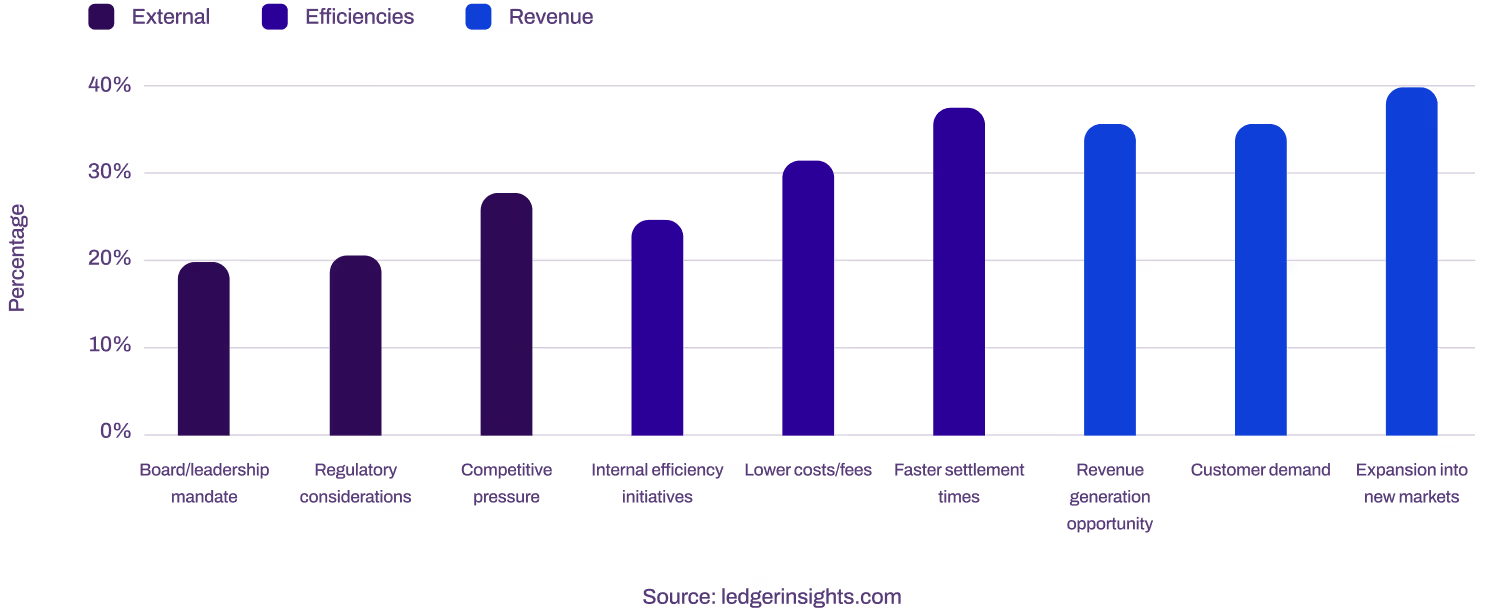

Across industries, enterprises are increasingly exploring stablecoins as part of broader financial modernization efforts. Enterprise inquiries related to stablecoin-enabled infrastructure increased more than fivefold from 2024 to 2025, driven primarily by the need for faster settlement, easier expansion into new markets, and new opportunities to generate revenue and improve capital efficiency.

Top factors influencing stablecoin exploration

Rather than replacing existing systems, most businesses are evaluating stablecoins as a way to address specific points of friction within the money-movement lifecycle, particularly where cross-border payments, liquidity management, FX, and treasury operations remain slow, costly or operationally complex.

Financial Institutions

Payment Acquirers

Card issuers

Trading & Investment Platforms

Travel & Airlines

Creator Economy

Global Merchants & Technology Companies

Remittance Companies

Payroll Providers

E-commerce & Marketplaces

Gaming

Import / Export Trade

Questions to guide your stablecoin strategy:

Payments, Liquidity & Timing

- Do you need to prefund accounts days in advance to support cross-border payments?

- Does payment timing influence how much cash you are required to hold in certain currencies or markets?

- Do banking hours, weekends, or cut-off times delay when funds can actually move?

Cross-Border Settlement

- Do international payments take days to settle, even when urgency is high?

- Does settlement speed vary significantly by corridor, bank or currency?

- Are funds received in one region slow to become usable elsewhere?

FX Fees

- Are FX fees or spreads meaningful at scale across cross-border flows?

- Do FX costs vary by corridor in ways that are difficult to predict or reconcile?

- Are your FX fees opaque and lack transparency as you move money globally?

Treasury Management & Idle Cash

- Do you move money frequently between regions, subsidiaries or legal entities?

- Is internal money movement slow, manual or constrained by timing windows?

- Does cash sit idle while waiting for settlement, reconciliation, or redeployment?

Regulation & Market Expansion

- Do payment or settlement requirements slow entry into new markets?

- Does regulatory uncertainty limit which payment or treasury solutions you can use?

If any of these challenges stand out for your business, stablecoins may be relevant for targeted payment or treasury workflows.

Are you ready for Velocity?

Solutions & Use Cases

Most finance teams build the case by looking at four dimensions:

Realtime Settlement

Description

Traditional payment rails often introduce delays between when a transaction is initiated and when funds are fully settled and usable. These delays can increase counterparty risk, complicate reconciliation, and constrain liquidity management.

Stablecoin-based settlement enables near-real-time transfer of value, allowing funds to move and settle continuously rather than in batches.

Benefits

- Shortens settlement cycles from days to minutes

- Reduces counterparty and settlement risk

- Improves liquidity availability and cash predictability

- Enables faster reconciliation and downstream payments

Send Money Anywhere, Anytime

Description

Cross-border payments are frequently constrained by banking hours, cut-off times, weekends, and local holidays. These constraints can slow operations, particularly for global platforms, marketplaces, and businesses operating across multiple time zones.

Stablecoin infrastructure allows money to move both instantaneously and continuously, independent of traditional banking schedules.

Benefits

- Enables 24/7/365 payment availability

- Removes dependency on local banking hours

- Improves reliability of global payouts and disbursements

- Supports international operations without timing constraints

Move Funds Within Your Global Entities

Description

Large organizations often move capital between subsidiaries, regions or legal entities to manage liquidity, fund operations and rebalance cash.

These internal transfers can be slow, manual, and operationally complex when routed through traditional banking rails.

Stablecoins provide a neutral, programmable layer for internal fund movement across borders.

Benefits

- Accelerates internal transfers between entities and regions

- Reduces reliance on multiple correspondent banking relationships

- Simplifies internal treasury operations and coordination

- Improves visibility into global liquidity positions

Reduce FX Friction

Description

Foreign exchange costs and complexity increase as businesses scale across markets. FX pricing can be opaque, vary significantly by corridor, and involve multiple intermediaries.

Stablecoins can act as a common settlement layer, reducing the number of FX conversions required and improving pricing transparency for cross-border flows.

Benefits

- Lowers FX spreads and intermediary fees at scale

- Improves transparency and predictability of FX costs

- Reduces operational overhead associated with multi-currency settlement

- Simplifies reconciliation across currencies and corridors

Unlock Yield

Description

In many organizations, cash sits idle while awaiting settlement, reconciliation or redeployment across accounts and regions. This idle liquidity represents an opportunity cost.

By shortening settlement cycles and centralizing liquidity, stablecoin-based infrastructure can enable more efficient use of working capital, including the ability to deploy excess balances into low-risk stablecoin yield strategies where appropriate.

Benefits

- Reduces idle cash trapped by settlement delays

- Improves capital efficiency across global treasury operations

- Enables optional yield generation on excess balances

- Enhances visibility into deployable liquidity

* Yield and rewards are generated by third-party issuers and protocol partners and are not offered, guaranteed, or underwritten by Velocity. Rates are variable and subject to change. Not available in all jurisdictions.

Eliminate Pre-Funding

Description

Many payment and payout models require businesses to prefund accounts in multiple jurisdictions to ensure timely execution.

This approach ties up capital, increases operational complexity, and limits flexibility. Stablecoins can enable just-in-time funding models, reducing the need to maintain excess balances across regions.

Benefits

- Reduces capital tied up in prefunded accounts

- Improves working capital efficiency

- Simplifies treasury structures across jurisdictions

- Increases flexibility in managing global liquidity

Compliance Considerations

Stablecoins are only as useful as the regulatory framework supporting them. In 2026, the key question is no longer “are stablecoins regulated?”, it’s where, how, and under which license.

Regulation Is Unlocking Enterprise Flows

Regulatory uncertainty was the biggest blocker to adoption

That blocker is now largely removed.

- 25+ countries have introduced stablecoin or digital asset regulation

- Clear frameworks now exist across the EU (MiCA), UK (FSMA), Singapore and US

- Financial institutions are actively expanding stablecoin offerings in response to corporate demand

Regulation has shifted stablecoins from “alternative rails” to credible payment infrastructure.

When assessing a provider or approach, ask:

- Is the provider operating under recognised payments or e-money frameworks?

- Are fiat on/off-ramps regulated in the jurisdictions you operate in?

- Who holds customer funds, and under what legal structure?

- How are AML, sanctions screening, and transaction monitoring handled?

- Can the setup scale across regions without re-architecting compliance?

Geographic coverage plus regulatory depth are a primary feature.

Velocity is building our regulatory roadmap to match our compliance-led approach with our network live in major global markets and rapid expansion underway.

%201.svg)

Implementation Checklist

The world is moving onchain. At Velocity, we believe that over the next 5-7 years the majority of B2B payments and settlement flows will move to stablecoin rails.

But this won’t happen all at once. Here’s a tactical approach to start small and expand as needed:

What Implementation Looks Like with Velocity

Velocity provides payment and related services involving stablecoins and other crypto-assets. While stablecoins are designed to maintain a stable value by reference to a fiat currency or other assets, they are not risk-free. Stablecoins may be subject to de-pegging events, liquidity constraints, issuer or reserve-related risks, operational failures, and changes in regulatory treatment, which may result in losses or delays in redemption. The value and functionality of stablecoins may be affected by factors outside of Velocity’s control, including market conditions, actions or inactions of issuers, custodians, or third-party service providers, and disruptions to underlying blockchain networks. You may lose some or all of the value transferred or held using stablecoins. Velocity operates in multiple jurisdictions and certain services may be restricted in your location. Past performance, illustrative examples, or forward-looking statements do not constitute reliable indicators of future outcomes. Before using Velocity’s services, you should ensure that you fully understand the risks involved and carefully consider whether such services are appropriate for you in light of your objectives, financial situation, knowledge, and risk tolerance. You should seek independent professional advice where appropriate. This presentation is provided for informational purposes only, is intended for review of a professional institution and does not constitute investment advice, a financial promotion, solicitation, or a binding offer to provide services. Any services referenced are subject to applicable regulatory requirements, eligibility criteria, and contractual documentation.

Ready for Velocity?

Money that moves like the internet: instant, global, flexible. With settlement, payments, treasury, and FX in one platform.