Treasury Was Built for a World With Opening Hours

For decades, moving money across borders meant planning around delay. Settlement windows closed at a certain hour. Correspondent chains took their time. If you were running a multi-entity business, you prefunded subsidiaries, overcapitalised where you had to, and held excess liquidity in places where getting it out quickly was either expensive or uncertain. Once money left your account, it was gone for a few days.

That wasn't poor management or bad treasury. It was the only sensible way to operate within the rails that existed. But it also baked in a lot of structural inefficiency that nobody questioned, because there wasn't much point questioning something you couldn't change.

The Cost of Slow Capital

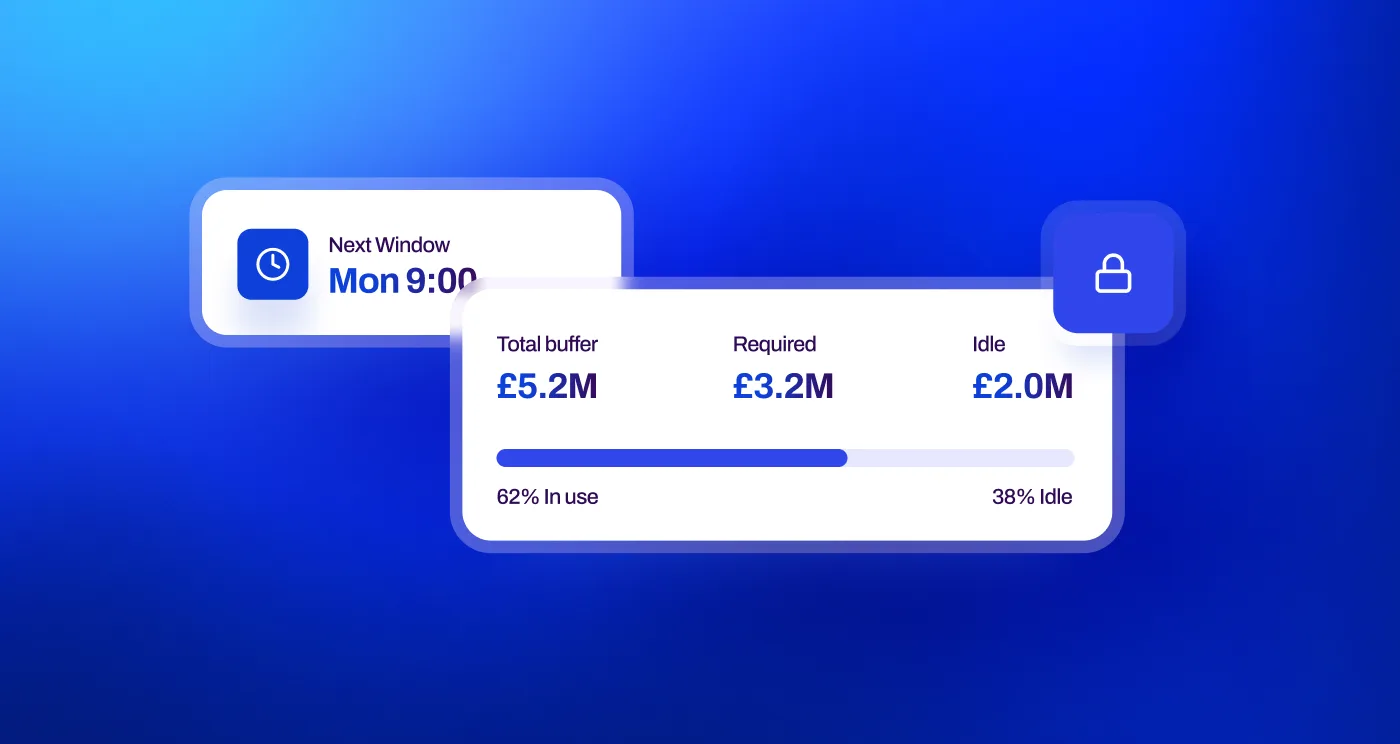

That gap has real consequences. When capital takes days to reposition, treasury teams compensate by holding more of it. Cash accumulates in one entity while another leans on a credit line. Buffers sit idle because you cannot risk being short. Working capital stretches not because the business is inefficient, but because the rails are.

The cost of that inefficiency is easy to underestimate until you look at it properly. When capital takes days to reposition, you compensate by holding more of it. Cash piles up in one entity while another draws down a credit line. Buffers sit there doing nothing because the alternative, being short, isn't an option. Working capital stretches, and it stretches not because the business is badly run but because the plumbing underneath it is slow.

Meanwhile the environment around treasury has changed completely. Markets don't wait for banking hours. FX moves while finance teams sleep. Customers transact across time zones without giving a thought to where anyone's bank happens to sit. Revenue gets recognised instantly, platforms reconcile continuously, and commerce genuinely never stops. Liquidity, though, often still does. That mismatch is getting harder to justify.

Why Stablecoins Are Entering the Conversation

This is why stablecoins are showing up in serious treasury conversations now, and not the kind of conversations they were showing up in two or three years ago. Treasury isn't chasing novelty. It never has. The function exists to manage risk, preserve capital, and keep control. What's changed is that stablecoins now let settlement happen at the speed the rest of the business already runs at. When value moves globally in minutes instead of days, liquidity stops being something you park defensively and starts being something you can actually manage.

That shift changes the economics. If you can mobilise capital when you need it, you don't have to structurally overcapitalise every entity on the off chance. Intercompany funding gets more fluid. Cross-border obligations stop requiring heavy prefunding. Credit lines go back to being strategic tools rather than something you're leaning on because the rails let you down. Capital that used to sit idle gets deployed intentionally. Short-term instruments become accessible without the settlement-lag anxiety. Yield strategies, where policy allows, get easier because the liquidity is actually reachable.

Speed Without Governance Is Just Faster Risk

None of that matters, though, if the governance doesn't hold up. Speed on its own isn't a virtue in treasury, it's a liability. Digital liquidity only works at institutional scale when it meets the same bar as fiat: dual approvals, segregation of duties, clean reconciliation into the ERP, audit trails that survive scrutiny, defined counterparty exposure, legal clarity on custody and redemption. If those controls are not embedded, the infrastructure is not ready for institutional balance sheets, as liquidity is only valuable if it is governed. Without that, faster settlement simply introduces faster risk.

The Questions Treasury Is Actually Asking

The questions treasury teams are asking now reflect that. A few years ago the conversation was mostly about yield. Today, yield remains relevant, but it sits within a broader discussion about liquidity management and capital efficiency. Can we cut trapped liquidity across subsidiaries? Can we tighten the working capital cycle? What does continuous settlement actually do to FX timing risk? How do we stay in control in a 24/7 environment, and what happens under stress? These aren't fringe digital asset debates. They're core treasury questions.

Regulatory clarity is also reinforcing this shift. Clear rules on issuance standards, reserves, supervision, and redemption don't slow any of this down, they're what makes it possible. Once boards and auditors have defined guardrails to point at, the conversation moves on from whether this is allowed to how to structure it properly.

A Layered Future, Not a Binary One

None of this means banks go away. They're still the foundation. Credit facilities, fiat accounts, traditional rails, they all continue to anchor corporate finance and they're not going anywhere. What's emerging is a layered system, not a replacement one. Digital dollars sit alongside everything else as another tool, particularly useful for cross-border flows and internal treasury movements, integrated into existing governance rather than bolted on outside it.

The benefits are boring and pragmatic, which is exactly what you want in treasury. Less prefunding. Smaller idle balances. Fewer intermediaries taking a cut. Better visibility across entities. Working capital that moves with the business instead of dragging behind it.

The shift isn't ideological. It's operational. In a world that never closes, liquidity can't keep running on infrastructure built for one that did. Treasury's mandate hasn't changed. The systems underneath it just need to catch up.